Introduction to Mortgage-Backed Securities

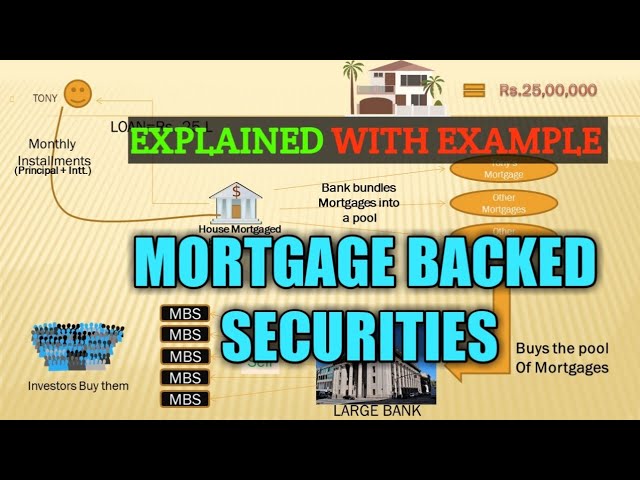

Mortgage-backed securities (MBS) are a type of financial asset that is secured by a collection of mortgages. These securities are created by pooling together a group of similar home loans, which are then sold to investors. MBS can be considered as bonds that are backed by mortgage loans, which are typically residential in nature. They play a crucial role in the housing finance system and the broader financial markets.

Creation and Structure

The process of creating an MBS involves several steps:

- Origination: This is the initial step where lenders provide home loans to borrowers for purchasing residential properties. These loans are typically standard mortgage agreements where the borrower agrees to repay the borrowed amount with interest over a set period, usually 15 or 30 years.

- Pooling: Once a sufficient number of similar mortgages are originated, they are pooled together by financial institutions. This pool of mortgages serves as the underlying asset for the mortgage-backed security.

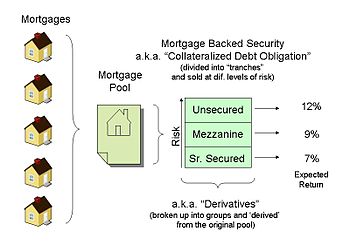

- Securitization: The pooled mortgages are then securitized, meaning they are packaged into securities that can be sold to investors. This process involves dividing the pool into smaller pieces called tranches, each with different levels of risk and return. This creates a diversified investment opportunity for investors.

- Issuance: The newly created MBS are issued to investors. These securities are usually sold through public offerings or private placements. They come with different ratings assigned by credit rating agencies, reflecting the level of risk associated with each tranche.

Types of Mortgage-Backed Securities

There are several types of MBS, each with its characteristics and risk profiles:

- Pass-Through MBS: In this type, the principal and interest payments made by the mortgage borrowers are “passed through” to the MBS investors. Pass-through MBS are the simplest form and are typically created by pooling fixed-rate mortgages.

- Collateralized Mortgage Obligations (CMOs): CMOs are more complex than pass-through MBS. They are structured into multiple tranches, each with different maturity dates and risk levels. This structure allows for greater customization and appeal to a broader range of investors. Tranches can be designed to cater to investors with varying risk appetites and investment horizons.

- Commercial Mortgage-Backed Securities (CMBS): While residential mortgages back most MBS, CMBS are backed by commercial real estate loans. These can include loans on office buildings, shopping centers, and other commercial properties.

Role in the Financial System

Mortgage-backed securities play a vital role in the financial system by providing liquidity to the mortgage market. Here’s how:

- Access to Capital: By selling mortgage-backed securities, lenders can free up capital, which they can then use to originate more loans. This creates a continuous cycle of lending and securitization, helping to maintain liquidity in the mortgage market.

- Risk Distribution: MBS allow the risk associated with mortgage loans to be spread across a broad base of investors. This diversification reduces the impact of any single mortgage default on the overall market.

- Investor Opportunities: MBS offer a variety of investment opportunities. Investors can choose from different tranches based on their risk tolerance and return expectations. This flexibility makes MBS attractive to a wide range of institutional and individual investors.

Risks and Challenges

Despite their benefits, mortgage-backed securities are not without risks and challenges:

- Credit Risk: This is the risk that borrowers will default on their mortgage payments. The credit quality of the underlying mortgages significantly impacts the MBS. If a significant number of borrowers default, the value of the MBS can decline.

- Interest Rate Risk: Changes in interest rates can affect the value of MBS. When interest rates rise, the value of existing MBS tends to fall because newer issues offer higher yields. Conversely, when rates fall, the value of existing MBS can increase.

- Prepayment Risk: This risk arises when borrowers pay off their mortgages early, usually when interest rates decline, and refinancing becomes attractive. Early repayment can reduce the expected interest payments to MBS investors, affecting their returns.

- Complexity and Transparency: The complexity of certain MBS structures, especially CMOs, can make it difficult for investors to understand the risks fully. Lack of transparency regarding the quality of the underlying mortgages can also pose significant risks.

The Role of Government-Sponsored Enterprises (GSEs)

Government-sponsored enterprises, such as Fannie Mae (Federal National Mortgage Association) and Freddie Mac (Federal Home Loan Mortgage Corporation), play a significant role in the MBS market. These GSEs purchase mortgages from lenders, pool them, and issue MBS. They provide a guarantee on the timely payment of principal and interest, which enhances the credit quality of MBS and makes them more attractive to investors.

Historical Context and the Financial Crisis

The role of MBS in the 2007-2008 financial crisis cannot be overstated. Leading up to the crisis, there was a significant increase in the issuance of subprime MBS, which were backed by high-risk mortgages. When the housing market collapsed, the defaults on these mortgages soared, leading to massive losses for investors holding subprime MBS. This contributed to the broader financial meltdown and highlighted the need for better regulation and transparency in the MBS market.

Regulation and Reforms

In the aftermath of the financial crisis, several regulatory reforms were implemented to address the issues associated with MBS:

- Dodd-Frank Act: This comprehensive piece of legislation aimed to increase transparency and accountability in the financial industry. It included provisions for stricter oversight of the MBS market and the institutions involved in securitization.

- Qualified Residential Mortgage (QRM) Standards: These standards were introduced to ensure that only high-quality mortgages could be securitized without requiring the issuer to retain a portion of the credit risk.

- Enhanced Disclosure Requirements: New regulations required greater transparency in the securitization process, including detailed information about the underlying mortgages and the performance of the MBS.

Conclusion

Mortgage-backed securities are a critical component of the financial system, providing liquidity to the mortgage market and offering investment opportunities to a wide range of investors. However, they also come with significant risks, as highlighted by the financial crisis. Understanding these risks and the role of regulatory reforms is essential for investors and policymakers alike.

I hope this detailed overview of mortgage-backed securities provides you with a comprehensive understanding. If you have any specific questions or need more details on any aspect, feel free to ask!