An Individual Retirement Account (IRA) is a tax-advantaged savings plan available in the United States, designed to help individuals save for retirement. Offered by various financial institutions like banks, brokerages, and credit unions, these accounts act as a trust holding investment assets purchased with a taxpayer’s earned income for their eventual use in old age. While initially designed for self-employed individuals without access to workplace retirement plans like 401(k)s, anyone with earned income can open and contribute to an IRA, even if they participate in an employer-sponsored plan. Income from sources like interest, dividends, or Social Security does not qualify as earned income for contribution purposes.

How IRAs Work

IRAs allow individuals to invest funds over the long term for retirement. You can open an IRA through banks, investment companies, online brokerages, or personal brokers. These accounts typically offer a wide range of investment options, including stocks, bonds, exchange-traded funds (ETFs), and mutual funds. Self-Directed IRAs (SDIRAs) provide even broader options, allowing investment in assets like real estate and commodities, though the riskiest investments are generally prohibited.

A key feature of IRAs is their tax-advantaged status. Contributions may be tax-deductible, earnings within the account typically grow tax-free or tax-deferred, and withdrawals in retirement are taxed according to the specific type of IRA. Because IRAs are intended for long-term retirement savings, withdrawals before the age of 59½ usually incur a 10% penalty tax, in addition to any regular income tax due on the withdrawn amount. However, exceptions to this penalty exist for certain circumstances, such as funding qualified educational expenses or making a first-time home purchase.

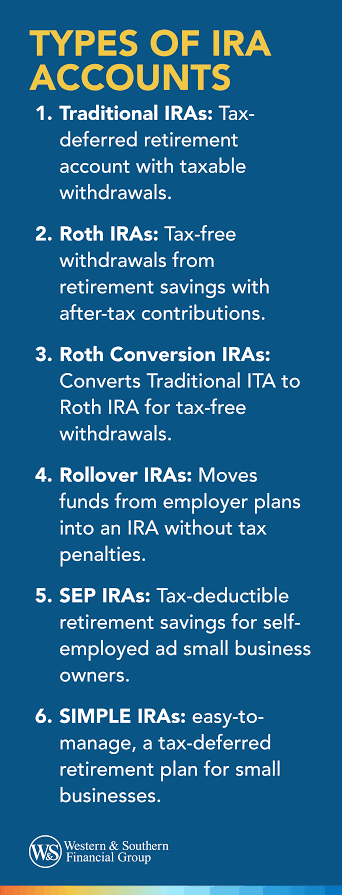

Types of IRAs

Several types of IRAs exist, each with distinct rules regarding eligibility, taxation, and withdrawals:

- Traditional IRA: Contributions to a Traditional IRA are often tax-deductible, meaning they can lower your taxable income in the year you contribute. The deductibility depends on whether you (or your spouse) are covered by a retirement plan at work and your modified adjusted gross income (MAGI). For 2024, if covered by a workplace plan, contributions are fully deductible for single filers with MAGI below $77,000 and married couples filing jointly with MAGI below $123,000 (limits increase slightly for 2025). If not covered by a workplace plan, contributions are fully deductible regardless of income. Investments within a Traditional IRA grow tax-deferred, meaning you don’t pay taxes on earnings until you withdraw the money in retirement. Withdrawals in retirement are taxed as ordinary income. Anyone with earned income can contribute, regardless of age. Required Minimum Distributions (RMDs) generally must begin at age 73.

- Roth IRA: Contributions to a Roth IRA are made with after-tax dollars and are not tax-deductible. Investments grow tax-free, and qualified withdrawals in retirement (generally after age 59½ and after the account has been open for five years) are completely tax-free. Contributions (but not earnings) can be withdrawn tax-free and penalty-free at any time. Eligibility to contribute to a Roth IRA is subject to income limitations. Like the Traditional IRA, there is no age limit for contributions, provided you have earned income and meet the income requirements. Roth IRAs do not have RMDs during the original owner’s lifetime.

- SEP IRA (Simplified Employee Pension): This plan allows employers, typically small businesses or self-employed individuals, to make contributions to Traditional IRAs set up for their employees (or for themselves). Employers make contributions directly into the employee’s SEP IRA.

- SIMPLE IRA (Savings Incentive Match Plan for Employees): Available to small businesses without other retirement plans, this IRA allows both employee and employer contributions. Employers are required to make either matching contributions (up to 3% of employee compensation) or non-elective contributions (2% of compensation) for eligible employees. It functions similarly to a 401(k) but has lower contribution limits and simpler administration.

- Rollover IRA: This isn’t a separate type of contribution account but rather a Traditional or Roth IRA used to receive funds transferred (“rolled over”) from an employer-sponsored retirement plan like a 401(k). Rolling over funds allows them to continue growing tax-advantaged and may offer more investment choices or lower fees compared to the previous plan. A rollover involves moving assets from one retirement plan to another tax-free.

- Other IRAs: Other variations include Inherited (or Beneficiary) IRAs, for individuals who inherit an IRA; Custodial IRAs, set up for minors with earned income; and Conduit IRAs, traditional IRAs funded solely by transfers from qualified plant. The myRA, a government-bond-only Roth-based IRA introduced in 2014, was phased out in 2017.

Benefits of IRAs

IRAs offer significant advantages for retirement savers:

- Tax Advantages: Both Traditional and Roth IRAs provide tax benefits. Traditional IRAs offer potential upfront tax deductions, reducing current taxable income. Roth IRAs offer tax-free withdrawals of contributions and earnings in retirement.

- Tax-Free or Tax-Deferred Growth: Investments held within both Traditional and Roth IRAs grow without being taxed annually on dividends or capital gains. For Traditional IRAs, taxes are deferred until withdrawal; for Roth IRAs, qualified withdrawals are entirely tax-free.

- Investment Flexibility: Compared to many employer-sponsored plans like 401(k)s, IRAs generally offer a wider array of investment choices, including individual stocks, bonds, ETFs, and mutual funds.

- Accessibility: IRAs are available to anyone with earned income, regardless of whether they have a workplace retirement plan. They are relatively easy to set up through various financial institutions.

- Individual Control: As the name suggests, these are individual accounts, giving the owner control over investment decisions and withdrawal strategies (within IRS rules).

Disadvantages and Limitations

Despite their benefits, IRAs also have limitations:

- Contribution Limits: Annual contribution limits for IRAs are significantly lower than those for workplace plans like 401(k)s. For 2024 and 2025, the maximum contribution is $7,000 per year, with an additional $1,000 catch-up contribution allowed for individuals aged 50 and over.

- Early Withdrawal Penalties: Taking funds out before age 59½ typically results in a 10% penalty on the withdrawn amount, plus applicable income taxes (for Traditional IRA withdrawals or Roth IRA earnings). This makes IRAs less suitable for short-term savings needs.

- Income Restrictions: Eligibility to deduct Traditional IRA contributions can be phased out based on income if covered by a workplace plan. Similarly, the ability to contribute to a Roth IRA is phased out and eliminated at higher income levels. Traditional IRAs have no income limit for making contributions, only for deducting them.

- Required Minimum Distributions (RMDs): Traditional IRA holders must start taking withdrawals (RMDs) annually beginning at age 73. These distributions are taxed as ordinary income. Roth IRAs do not have RMDs for the original owner.

Contribution Rules and Multiple IRAs

To contribute to any IRA, an individual must have earned income for the year. You can have multiple IRA accounts, such as both a Traditional and a Roth IRA. However, the total amount contributed across all your Traditional and Roth IRAs cannot exceed the annual maximum limit ($7,000 for 2024/2025, or $8,000 if age 50+). For example, if an individual under 50 contributes $2,000 to a Traditional IRA in 2024, they can only contribute up to $5,000 more to a Roth IRA (or any other combination of Traditional/Roth IRAs) for that year.

IRAs serve as powerful tools for individuals seeking to build long-term savings for retirement, offering valuable tax benefits and investment flexibility. Understanding the different types, rules, and limitations is crucial for utilizing them effectively as part of a comprehensive retirement strategy.