A Certificate of Deposit (CD) is a type of savings account offered by banks and credit unions where a fixed amount of money is deposited for a predetermined period, known as the term. In exchange for agreeing to keep the funds locked away for this term, the financial institution pays a fixed interest rate, which is typically higher than rates offered on traditional savings or money market accounts. This makes CDs a relatively safe and conservative investment option compared to stocks or bonds, offering predictable growth but less flexibility and lower potential returns than riskier assets. Credit unions often refer to their version of CDs as share certificates.

How Certificates of Deposit Work

Opening a CD involves an agreement between the depositor and the financial institution. Key factors define how a CD operates:

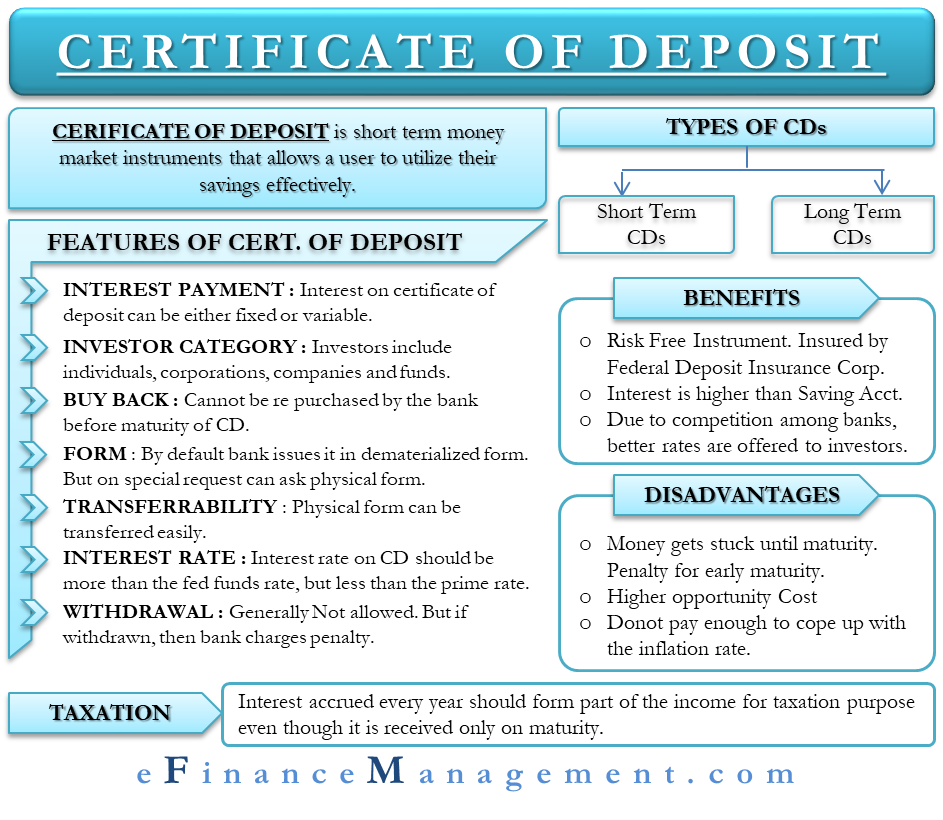

- Principal: This is the fixed amount of money you deposit when opening the CD. In some markets, like India, there’s a specific minimum deposit requirement, often starting at Rs. 1,00,000 or multiples thereof.

- Term: This is the agreed-upon length of time the funds must remain deposited to earn the stated interest rate without penalty. Common terms range from three months to five years, although shorter and longer terms (like 10 years) are also available. The term concludes on the maturity date.

- Interest Rate (APY): CDs typically offer a fixed annual percentage yield (APY) for the entire term, meaning the rate won’t change even if market rates fluctuate. This guaranteed rate provides predictable returns. Some specialty CDs might have variable rates. Interest earned is usually compounded and added to the CD balance, often monthly or quarterly. Disclosure statements should specify if the rate is fixed or variable, when interest is paid (e.g., monthly, semi-annually), and how it’s paid (e.g., check, electronic transfer).

- Maturity: When the CD reaches its maturity date, the term ends, and the depositor can withdraw the principal plus all accrued interest without penalty.

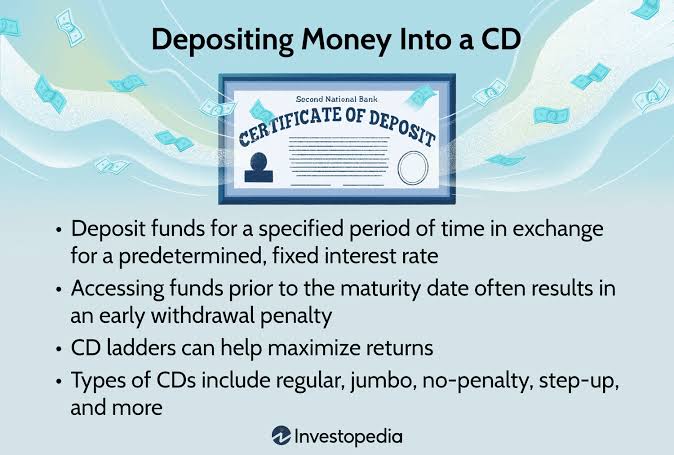

- Early Withdrawal Penalty (EWP): If you need to access your funds before the CD matures, you will almost always face an early withdrawal penalty. The specific penalty varies by institution but usually involves forfeiting a portion of the interest earned.

- Renewal: Financial institutions set policies regarding what happens at maturity, including whether the CD automatically reinvests (renews) for another term if the depositor doesn’t provide instructions.

Key Features of CDs

Certificates of Deposit possess several distinct characteristics:

- Higher Interest Rates: Generally, CDs offer better interest rates than standard savings accounts as compensation for the lack of liquidity. The best rates can be significantly higher than national averages.

- Guaranteed Returns: The fixed interest rate ensures a predictable return over the CD’s term, shielding the investment from market volatility. This makes CDs suitable for risk-averse savers with specific goals like saving for a down payment or a wedding.

- Safety and Insurance: CDs are considered one of the safest savings options. In the U.S., funds in CDs at federally insured banks (FDIC) or credit unions (NCUA) are typically insured up to $250,000 per depositor, per institution, per account ownership category. This insurance covers the total amount held across all accounts in your name at that bank, not each individual CD.

- Term Flexibility: CDs come in various term lengths, allowing investors to choose one that aligns with their investment horizon and financial goals. Some institutions offer a wider range of terms, from short (e.g., 3 months) to long (e.g., 5 or 10 years).

- Minimum Deposit: While varying by institution, some CDs, particularly in markets like India, have substantial minimum deposit requirements (e.g., Rs. 1 lakh).

- Issuers: In India, CDs are typically issued by Scheduled Commercial Banks (SCBs) and specific All-India Financial Institutions (FIs), governed by the Reserve Bank of India (RBI). SCB-issued CDs often have terms from 3 months to 1 year, while FI-issued CDs might range from 1 to 3 years.

- Transferability: CDs issued in dematerialized (electronic) form can sometimes be transferred through endorsement or delivery, similar to other securities, enhancing liquidity somewhat.

- Taxation: Interest earned on CDs is generally considered taxable income in the year it is earned.

Advantages of CDs

- Higher Yields than Savings: Offer potentially higher interest rates compared to traditional savings accounts.

- Safety: Principal is protected, and deposits are typically federally insured up to certain limits.

- Predictability: Fixed rates provide a guaranteed return, making financial planning easier.

- Variety of Terms: Choice of terms allows alignment with different savings timelines.

- Capital Preservation: Protects the initial investment amount.

Disadvantages of CDs

- Limited Liquidity: Significant penalties usually apply for withdrawing funds before maturity, making the money inaccessible for the term’s duration.

- Lower Growth Potential: Offer lower returns compared to potentially higher-growth, but riskier, investments like stocks and bonds.

- Inflation Risk: The fixed return might not keep pace with inflation, potentially eroding the real value (purchasing power) of your savings over time.

- Interest Rate Risk: If interest rates rise significantly after you lock into a CD, you miss out on earning the higher prevailing rates until your CD matures.

Specialty and Brokered CDs

Beyond traditional fixed-rate CDs, some institutions offer variations like:

- No-Penalty CDs: Allow withdrawal before maturity without penalty, usually offering slightly lower rates.

- Step-Up/Bump-Up CDs: Offer the option to increase the interest rate one or more times during the term if the institution’s rates rise.

CDs can also be purchased through brokerage firms or independent salespeople, known as deposit brokers. These “brokered CDs” might sometimes offer higher negotiated rates because the broker brings a large volume of deposits to the bank. However, it’s crucial to thoroughly vet the deposit broker and the issuing institution, as brokers are not typically licensed or certified by regulatory agencies. Checking the background and disciplinary history of brokers (through FINRA, SEC, or state regulators) and the reputation of the issuing bank is essential.

Eligibility and Loans

Eligibility to invest in CDs can vary, but generally includes individuals, corporations, companies, and funds. In India, Non-Resident Indians (NRIs) may invest on a non-repatriable basis. While banks and financial institutions generally cannot grant loans secured by their own CDs or buy back their own CDs before maturity, depositors might be able to obtain loans against their CDs, subject to specific permissions or restrictions (e.g., by the RBI in India).